The Business Model Canvas (BMC) serves as a strategic management template for developing new business models or documenting existing ones. While many stakeholders focus heavily on value propositions and customer segments, the Cost Structure block remains the foundation of financial viability. Without a disciplined approach to managing costs, even the most innovative value proposition can fail due to unsustainable expenditure. This guide explores the mechanics of cost management within the BMC framework, providing a detailed look at how organizations can align their financial architecture with their strategic goals.

📊 Understanding the Cost Structure Block

The Cost Structure represents the most important costs incurred to operate a particular business model. It is not merely a list of expenses but a reflection of the underlying economics of the enterprise. Every decision made in other blocks of the canvas—such as key activities, key resources, and partnerships—has a direct financial implication. Understanding this block requires moving beyond simple accounting to view costs as strategic levers.

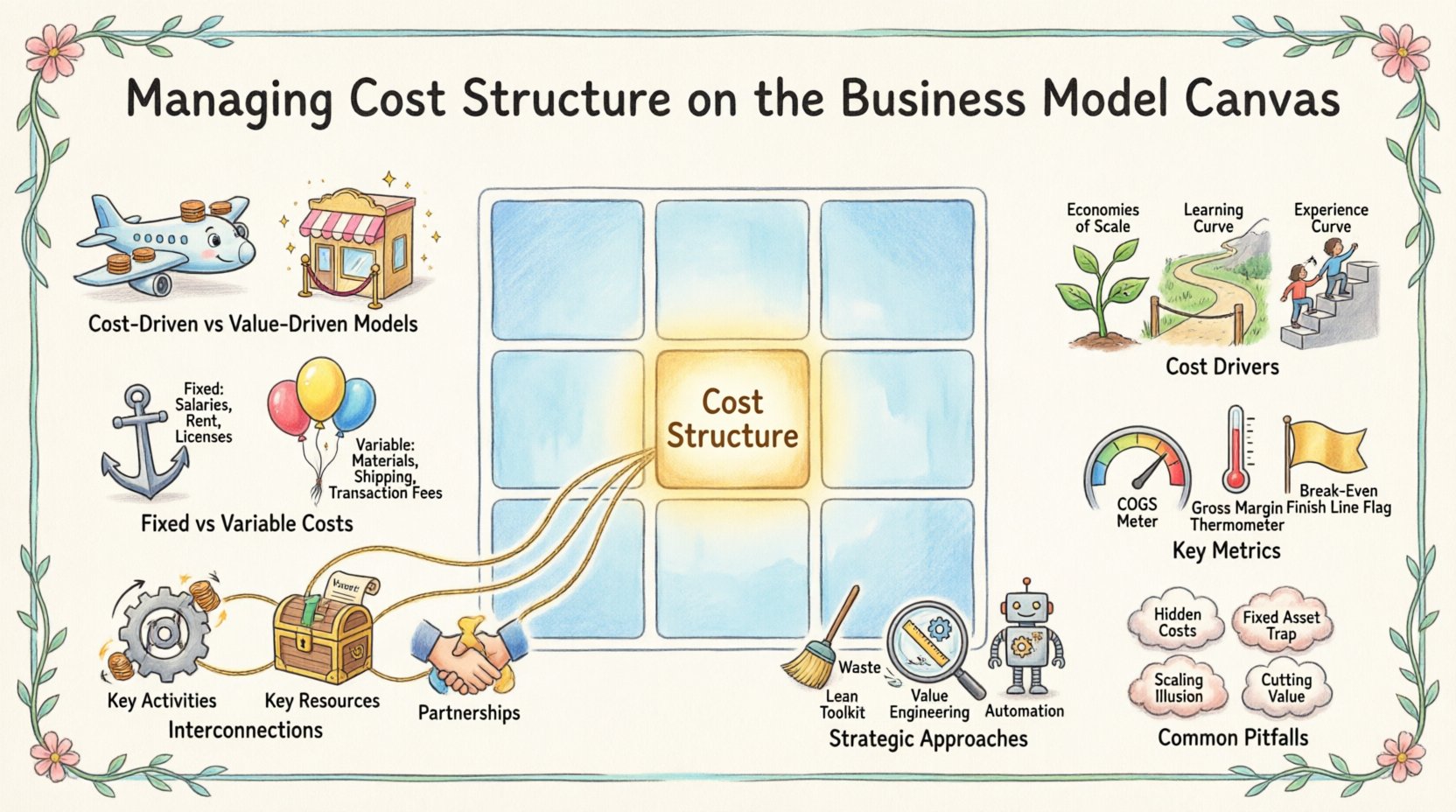

- Cost-Driven Models: These models focus on minimizing costs wherever possible. The goal is often low price, high volume, and automation. Think of budget airlines or discount retailers.

- Value-Driven Models: These models prioritize creating premium value, often accepting higher costs to deliver unique features, exceptional service, or superior quality. Luxury goods and specialized consulting firms often follow this path.

When analyzing the Cost Structure, one must consider the relationship between revenue and expenditure. A healthy business model ensures that the cost of acquiring and serving a customer is lower than the revenue generated by that customer over their lifetime. This balance is critical for long-term sustainability.

⚖️ Fixed vs. Variable Costs in Business Modeling

A fundamental distinction in managing cost structures is separating fixed costs from variable costs. This distinction dictates how a business scales and how much risk it bears during downturns.

Fixed Costs

Fixed costs remain constant regardless of the volume of goods or services produced. These are often associated with infrastructure and overhead.

- Salaries: Core management and administrative staff.

- Rent and Leases: Physical office space or warehouse facilities.

- Depreciation: Wear and tear on equipment and machinery.

- Licenses and Subscriptions: Ongoing fees for necessary operational tools.

High fixed costs can create a barrier to entry for competitors but also increase risk. If sales drop, the business must still pay these obligations. This requires a high break-even point, meaning significant sales volume is needed before profitability begins.

Variable Costs

Variable costs change in proportion to how much a company produces or sells. These costs are often more flexible and can be adjusted more easily when market conditions shift.

- Raw Materials: Inputs required to create the product.

- Shipping and Logistics: Costs associated with delivering the product to the customer.

- Transaction Fees: Payment processing charges per sale.

- Production Labor: Hourly wages tied directly to output.

Businesses with high variable costs and low fixed costs are often more agile. They can scale down quickly if demand decreases without being burdened by heavy overhead. However, they may face higher marginal costs per unit as they grow, potentially limiting margins at scale.

🔗 Interdependencies with Other Canvas Blocks

The Cost Structure does not exist in isolation. It is deeply interconnected with the other eight building blocks of the Business Model Canvas. A shift in one area inevitably impacts the financial structure.

1. Key Activities and Costs

The specific activities a company performs drive the majority of its costs. For example, a software company incurs high costs related to research and development (R&D), whereas a logistics company incurs high costs related to fleet maintenance and fuel.

- Production Activities: Manufacturing costs, assembly lines, and quality control.

- Problem-Solving Activities: Consulting time, support tickets, and troubleshooting.

- Platform/Network Activities: Server hosting, bandwidth, and maintenance for digital platforms.

Optimizing these activities is essential. If a key activity can be automated, the variable cost per unit may decrease, or the fixed cost of labor may shift to the fixed cost of technology.

2. Key Resources and Costs

Resources are the assets required to make the business model work. The type of resources dictates the cost profile.

- Physical Resources: Factories, vehicles, and inventory. These require capital investment and maintenance.

- Intellectual Resources: Patents, copyrights, and brands. These often involve upfront R&D costs but low marginal costs for replication.

- Human Resources: Talent acquisition and training. High-skill labor commands higher wages.

- Financial Resources: Cash flow, credit lines, and capital.

3. Key Partnerships and Costs

Outsourcing is a common strategy for managing cost structure. By partnering with external entities, a company can convert fixed costs into variable costs.

- Non-Core Activities: Outsourcing customer support or manufacturing can reduce overhead.

- Suppliers: Negotiating better terms with suppliers directly reduces the cost of goods sold.

- Alliances: Joint ventures can share the burden of large investments.

However, reliance on partners introduces risks. If a supplier raises prices or a partner fails to deliver, the cost structure becomes volatile.

📉 Key Cost Drivers

Cost drivers are the factors that cause a cost to increase or decrease. Identifying these drivers allows management to control costs more effectively.

- Economies of Scale: As production volume increases, the cost per unit typically decreases due to spreading fixed costs over more units.

- Economies of Scope: Costs decrease when producing a variety of products using the same resources.

- Learning Curve: Efficiency improves over time as workers become more proficient, reducing labor hours per unit.

- Experience Curve: Similar to learning curves but applies to the entire organization, including process improvements and technology adoption.

Understanding these drivers helps in forecasting. If a business expects a 50% increase in sales, they must anticipate how these drivers will affect their total expenditure.

🛠️ Strategic Cost Management Approaches

Once the costs are understood, the next step is optimization. This does not mean cutting costs indiscriminately, but rather aligning spending with value creation.

Lean Operations

The principles of lean management focus on eliminating waste. Every activity that does not add value from the customer’s perspective is a candidate for reduction.

- Inventory Reduction: Holding less stock reduces storage and insurance costs.

- Process Simplification: Removing unnecessary steps in production or service delivery.

- Just-in-Time: Ordering materials only as they are needed for production.

Value Engineering

This involves analyzing the function of a product or service to achieve the necessary performance at the lowest cost. It asks questions like: Does this feature justify its cost? Can a cheaper material achieve the same result without compromising quality?

Automation and Technology

Investing in technology can shift the cost structure. High initial investment in automation can lead to significantly lower variable costs in the long run. This is particularly relevant in manufacturing and data processing.

📏 Key Metrics for Cost Efficiency

To manage costs effectively, leaders must track specific metrics. These indicators provide a snapshot of financial health and efficiency.

- Cost of Goods Sold (COGS): Direct costs attributable to the production of goods sold. This includes labor and materials.

- Operating Expenses (OpEx): Costs not directly tied to production, such as marketing, administration, and R&D.

- Gross Margin: Revenue minus COGS. This indicates how efficiently a company produces its goods.

- Operating Margin: Revenue minus operating expenses. This shows how well the company manages its overhead.

- Break-Even Point: The level of sales at which total revenues equal total costs.

Regular review of these metrics ensures that the cost structure remains aligned with the business strategy. If margins shrink, it signals a need to adjust either the pricing strategy or the cost base.

🚧 Common Pitfalls in Cost Planning

Even with a clear framework, organizations often stumble when managing the Cost Structure block. Awareness of these common errors can prevent financial distress.

| Pitfall | Description | Impact |

|---|---|---|

| Underestimating Hidden Costs | Focusing only on direct costs while ignoring maintenance, training, or support. | Profit margins erode unexpectedly over time. |

| Over-Investing in Fixed Assets | Buying expensive equipment before demand is proven. | High overhead creates a high break-even point. |

| Ignoring Scaling Costs | Assuming costs remain linear as the business grows. | Costs may spike disproportionately during rapid growth. |

| Cutting Value-Adding Costs | Reducing spending on R&D or quality control to save money. | Product quality declines, leading to customer churn. |

1. The Fixed Cost Trap

Startups often commit to long-term leases or permanent staff before validating their business model. This creates a rigid cost structure that makes pivoting difficult. If the market shifts, the company is burdened by obligations it cannot meet.

2. The Hidden Expense Blindspot

Marketing costs are often underestimated. Customer acquisition costs (CAC) can be higher than anticipated if channels are saturated. Similarly, the cost of churn—losing a customer and having to replace them—can eat into profits if not factored into the model.

3. The Scaling Illusion

Many assume that doubling sales will simply double revenue without changing costs. However, scaling often requires new infrastructure, additional management layers, and expanded customer support. If the cost structure does not adapt to this growth, efficiency drops.

🔄 Final Considerations for Cost Optimization

Managing the Cost Structure is an ongoing process, not a one-time exercise. As the market evolves, so must the financial architecture of the organization. Regular audits of the Business Model Canvas ensure that the cost side remains balanced with the value side.

When revisiting the Cost Structure, consider the following questions:

- Are we paying for features customers do not value?

- Can we shift fixed costs to variable costs to increase flexibility?

- Are our partnerships optimizing our expense profile?

- Does our cost structure support our chosen competitive strategy?

A disciplined approach to cost management allows a business to remain resilient during economic downturns and agile enough to capitalize on new opportunities. By treating costs as a strategic asset rather than just a liability, organizations can build models that are robust, sustainable, and profitable over the long term.

The interaction between value creation and cost management is delicate. Too much focus on cutting costs can destroy the value proposition. Too little focus can drain the cash reserves. The goal is balance. By understanding the nuances of fixed and variable costs, the drivers of expenditure, and the interdependencies within the canvas, leaders can make informed decisions that secure the financial future of their enterprise.

Ultimately, the Business Model Canvas is a tool for thinking. When applied rigorously to the Cost Structure block, it provides clarity on where money goes and why. This clarity is the first step toward efficiency. With continued monitoring and adjustment, the cost structure can become a competitive advantage, enabling the organization to offer better prices or achieve higher margins than the competition.